Written by TFN Research Desk | covering startups, technology, venture capital, and business strategy.

While Blinkit and Zepto spent five years building India’s quick-commerce infrastructure, Peak XV waited. When it finally moved, it did not bet on groceries.

India’s most active venture firm sat out the entire first wave of quick commerce. Peak XV Partners, which is invested in 70% of India’s unicorns and made 81 investments in 2025 alone (Business Standard, December 2025), did not back Blinkit, Zepto, or Swiggy Instamart during the grocery dark store wars. That absence was a signal. In February 2026, the firm led a $15.3 million Series A into ZILO, a Mumbai-based fashion quick-commerce startup founded by former Flipkart and Myntra executives (YourStory, February 2026). The category: fashion delivered in under 60 minutes, with home trials included. The thesis: the infrastructure war is over. The vertical category war has begun.

Topic tags: Sector Analysis • Quick Commerce • Peak XV • Venture Capital • Indian Startup Strategy

The firm that sat out round one on purpose

Peak XV’s absence from the first quick-commerce wave was not oversight. It was a positioning choice rooted in the firm’s investment philosophy.

The first wave of Indian quick commerce was a capital-density game: who could build dark stores fastest, burn least per order, and hold on long enough for unit economics to mature. Blinkit, Zepto, and Swiggy Instamart competed on speed, geography, and cash. The investment thesis was infrastructure ownership, not category insight. That is not the kind of bet Peak XV characteristically makes.

The firm prefers entering when a category’s fundamentals are clear and the next layer of value creation is visible. In quick commerce, that moment arrived when Blinkit had proven Indian urban consumers would consistently pay for 60-minute delivery across categories. Once that behaviour was established, the question shifted: what else will they pay to receive in 60 minutes?

Fashion, it turns out, is a compelling answer. And Peak XV moved.

Why this story matters

Peak XV’s entry into quick commerce matters beyond one investment for three reasons.

First, a firm that has been invested in 70% of India’s unicorns (Business Standard, December 2025) does not make a first move in a major category without a developed thesis. The ZILO investment is not a test. It is a bet.

Second, the bet reveals what Peak XV believes comes after the infrastructure era. Horizontal platforms have built the dark store networks and consumer habits. The next decade of quick commerce will be won vertically: fashion, beauty, medicine, electronics, each with separate economics and separate customer psychology.

Third, for Indian founders building in adjacent spaces, understanding what Peak XV sees in ZILO is more useful than understanding the ZILO round itself. The specific investment is one data point. The thesis it reveals is a map.

Quick facts

| Metric | Value | Source |

|---|---|---|

| Firm | Peak XV Partners (formerly Sequoia Capital India) | Peak XV |

| Founded | 2006 | Peak XV |

| Headquarters | Bengaluru, India | Peak XV |

| AUM | Over $10 billion across India and Southeast Asia | Peak XV |

| 2025 investments | 81 | Tracxn, 2026 |

| Portfolio unicorn coverage | 70% of India’s unicorns | Business Standard, December 2025 |

| ZILO investment | $8 million in $15.3 million Series A, February 2026 | IndianWeb2, February 2026 |

| ZILO founders | Padmakumar Pal and Bhavik Jhaveri (ex-Flipkart, Myntra) | ZILO |

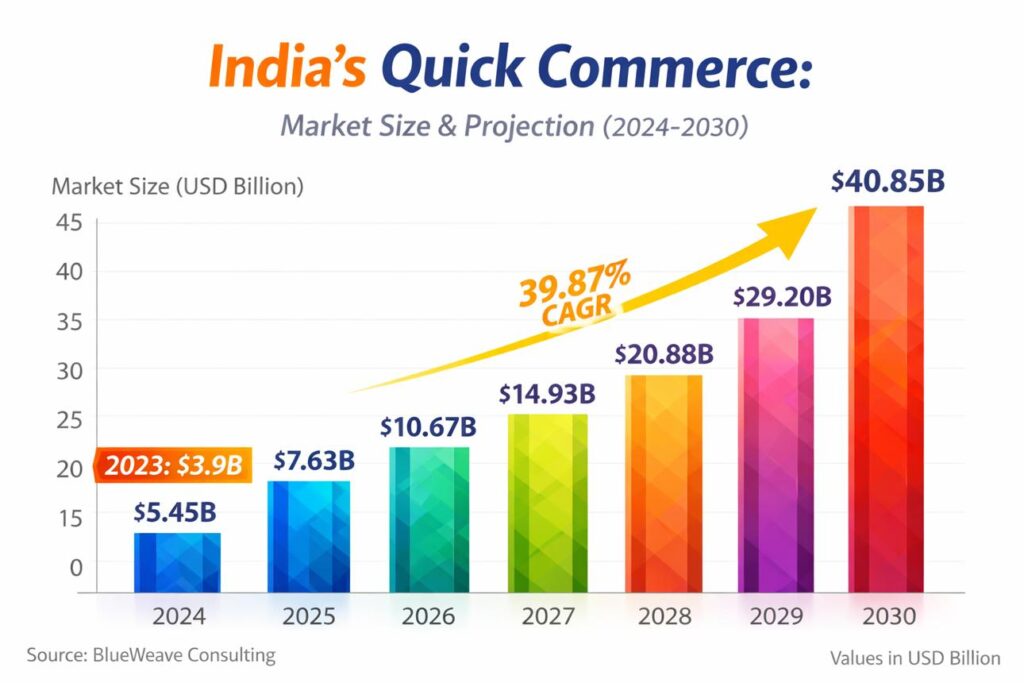

| India quick commerce market (FY24) | $3.3 billion | Outlook Business, 2025 |

Background

The Indian quick-commerce category emerged in earnest between 2020 and 2022, funded heavily by the behaviour shifts of the pandemic and the capital appetite of the global venture cycle. Zomato acquired Blinkit in 2022. Zepto raised at a $1 billion-plus valuation. Swiggy Instamart scaled aggressively on the back of Swiggy’s logistics infrastructure.

By FY24, the market had reached $3.3 billion in GMV, up from $0.5 billion in FY22 (Outlook Business, 2025). Blinkit held approximately 46% market share with 2,243 dark stores. The grocery war was largely decided. Survivors remained and the infrastructure was built.

ZILO was founded in 2025 by Padmakumar Pal and Bhavik Jhaveri, both executives who built their careers at Flipkart and Myntra, the two companies that defined Indian fashion e-commerce. Their premise was precise: deliver on-trend clothing from 200-plus brands within 60 minutes, with home trials included and instant returns available. The try-before-you-buy problem that physical retail solved and online commerce broke.

Peak XV first surfaced interest in ZILO in August 2025, when reports emerged it was considering a seed investment of approximately $5 million (Outlook Business, August 2025). By February 2026, it had led the Series A at $8 million, joined by InfoEdge Ventures and Chiratae Ventures at $2.5 million each (YourStory, February 2026). The angel cohort included Kunal Shah (CRED), Lalit Keshre (Groww), and Abhishek Bansal (Shadowfax), three operators whose presence signals category seriousness, not speculative interest.

Timeline

| Date | Milestone |

|---|---|

| FY22 | India quick-commerce market at $0.5 billion (Outlook Business, 2025) |

| 2022 | Zomato acquires Blinkit; Zepto crosses $1B valuation; grocery infrastructure war intensifies |

| 2024 | India quick-commerce market reaches $3.3 billion; Blinkit holds 46% share with 2,243 stores (Outlook Business, 2025) |

| 2025 | ZILO founded by ex-Flipkart and Myntra executives Padmakumar Pal and Bhavik Jhaveri |

| August 2025 | Reports emerge Peak XV is in talks to invest $5 million in ZILO’s seed round (Outlook Business, August 2025) |

| February 2026 | Peak XV leads $15.3 million Series A in ZILO; total round includes InfoEdge, Chiratae, and notable angel investors (YourStory, February 2026) |

How it happened

Shift 1: Infrastructure first, then verticalization

The strategic logic of Peak XV’s quick-commerce entry only makes sense in sequence. The first wave of Indian quick commerce had to happen before the second wave had anywhere to stand.

Blinkit and Zepto spent five years teaching urban Indian consumers a new behaviour: expect anything in under 60 minutes. That behaviour change required extraordinary capital investment in dark stores, logistics networks, and consumer education. It is the kind of investment that a category-defining vertical player like ZILO would not have survived making alone.

What ZILO benefits from is that the consumer habit is already formed. The dark store infrastructure in Mumbai exists. The logistical understanding of last-mile urban delivery is mature. ZILO does not need to teach customers to expect speed. Blinkit taught them that. ZILO needs to teach them that fashion is as logical a 60-minute category as groceries.

That is a materially easier problem. And it is the problem Peak XV is backing ZILO to solve.

Shift 2: Fashion as the highest-value vertical

Not every vertical is equal in quick commerce. The unit economics differ sharply by category. Grocery quick commerce works on high frequency and moderate basket sizes. The logic is volume over margin. Fashion works on high average order values, lower frequency, and higher emotional involvement per purchase.

Fashion also has a structural problem that quick commerce is uniquely positioned to solve. E-commerce broke the try-before-you-buy experience that physical retail had always offered. A shopper in a mall could try on five outfits and buy the one that fit. A shopper on Myntra would order three sizes and return two, creating friction, delay, and a logistical return chain that erodes margins.

ZILO’s model restores the physical retail experience at digital speed: 60-minute delivery, home trial, instant return if it does not work. The fashion category has high emotional stakes per purchase. A shopper unsure about an outfit would rather try it at home in 60 minutes than wait three days and then return it. That preference is the product.

The strategic move of adding celebrity stylist Anaita Shroff Adajania as Style Director and equity partner is also not decoration. It is a signal that ZILO is building a brand relationship with fashion, not just a delivery mechanism for SKUs. That distinction matters competitively.

Shift 3: Founder-market fit as the moat

The fashion quick-commerce category will attract competition. Slikk, KNOT, and Klydo are already operating in adjacent positions. Horizontal platforms including Blinkit and Zepto will eventually add fashion SKUs.

What none of them have is the founding team’s institutional knowledge. Padmakumar Pal and Bhavik Jhaveri built careers at the two companies that defined Indian fashion e-commerce. They understand brand relationships, inventory management for seasonal apparel, the psychology of the Indian fashion consumer, and the supply chain dynamics of fashion retail in ways that generalist operators simply do not.

In a category where brand curation and consumer experience are the differentiation, the people who know the brands and the consumers have an advantage that capital cannot easily replicate. That is the moat Peak XV is betting on alongside the category.

By the numbers

| Metric | Value | Source | Why it matters |

|---|---|---|---|

| Peak XV investments (2025) | 81 | Tracxn, 2026 | India’s most active VC still accelerating at scale |

| India quick commerce market (FY24) | $3.3 billion | Outlook Business, 2025 | Fourfold increase from $0.5B in FY22; consumer habit is real |

| ZILO Series A | $15.3 million led by Peak XV | YourStory, February 2026 | First major institutional fashion quick-commerce bet in India |

| ZILO delivery promise | Under 60 minutes with home trial and instant returns | ZILO | Differentiator that horizontal platforms structurally cannot replicate |

| Peak XV portfolio IPOs (Nov-Dec 2025) | Groww, Meesho, Pine Labs, Wakefit, Capillary Technologies | Peak XV via MEXC, 2025 | Five exits in two months; firm is deploying from a position of strength |

What competitors missed

Blinkit, Zepto, and Swiggy Instamart are building horizontally: adding SKUs across every category to increase order frequency and basket size. That strategy works for commodities where speed and price are the only variables. It does not work for fashion, where brand relationship, curation, and the emotional experience of buying clothes are the actual product.

The horizontal platforms missed a structural distinction. Fashion is not a category that fits neatly into a dark store inventory model designed for groceries. Apparel requires fit variety, seasonal rotation, brand curation, and the ability to handle high return rates without destroying margins. Those requirements need a vertical-first architecture from day one, not a horizontal platform’s attempt to add a fashion tab.

The broader investor community missed what Peak XV identified: quick commerce is not one business. It is an infrastructure layer that enables multiple vertical businesses, each with distinct economics, customer relationships, and competitive moats. The investor who waits for the infrastructure to mature and then backs the best vertical is not late. They are positioned precisely.

Risks and challenges

- Unit economics at early scale. Fashion quick commerce with home trials and instant returns carries a high operational cost per order. Return rates on apparel e-commerce in India can exceed 30%. If ZILO’s return economics are not managed tightly, the capital efficiency case deteriorates before the business reaches breakeven.

- Horizontal platform encroachment. Blinkit and Zepto have the dark store infrastructure, the consumer relationship, and the capital to add fashion as an SKU category. If they move aggressively on fashion verticalisation before ZILO reaches escape velocity, the standalone player gets squeezed.

- Brand acquisition cost. Curating 200-plus fashion brands requires relationship-building, minimum purchase commitments, and inventory risk. Brand supply chain management is materially harder than grocery supply chain management.

- Geography concentration. Fashion quick commerce economics work best in dense urban markets with high-value fashion consumers. Scaling beyond Mumbai and Bengaluru to Tier 2 cities requires a different unit economics model.

- Category education. While 60-minute grocery delivery is now mainstream, 60-minute fashion delivery with a home trial is a new consumer behaviour that still requires market education and habit formation.

What founders can learn

- Study where infrastructure already exists before building. ZILO is not building delivery infrastructure. It is building a fashion experience on infrastructure Blinkit already spent billions creating. Identify the behaviour that has already been formed in your category and build the next product on top of it.

- Domain expertise in the specific category is non-negotiable. ZILO’s founders built Flipkart and Myntra. That institutional knowledge is not a credential. It is the operational moat. A generalist founding team entering fashion quick commerce faces a different and harder problem.

- The second wave of any technology cycle is often more investable than the first. The first wave requires infrastructure capital and high risk tolerance. The second wave, vertical categories built on proven infrastructure, offers a clearer value creation path for investors and founders alike.

- Brand matters in fashion in a way it does not in groceries. Adding celebrity stylist Anaita Shroff Adajania as an equity partner is not marketing spend. It is a signal to brands and consumers that ZILO is building a fashion identity, not a delivery service.

Expert analysis

Bull case. Fashion is one of the highest-value, highest-frequency retail categories in India. The try-before-you-buy problem is real, persistent, and unsolved at speed. If ZILO can deliver that experience at 60 minutes with credible brand curation and workable return economics, it builds a category that no horizontal platform can replicate quickly. Peak XV’s backing provides runway to reach scale before the horizontal players mobilise.

Bear case. Fashion quick commerce is operationally complex in ways that grocery commerce is not. Returns are high, inventory is seasonal, and brand relationships require minimum commitments that create working capital pressure. If the per-order economics do not work at ZILO’s early scale, the fundraising story becomes harder before the category thesis can be proven. The competitive window is real but not unlimited.

Contrarian view. The more interesting question is not whether ZILO wins but whether standalone vertical quick-commerce players can win at all. Blinkit and Zepto have the infrastructure, the consumer trust, and the capital to add fashion as a category. If they move fast enough, they capture the demand without building a vertically specialised product. The real winners of the vertical quick-commerce era may be the horizontal platforms that add verticals, not the startups building them independently.

Future outlook

India’s quick-commerce market is entering its most consequential phase. The infrastructure era, the dark store race to own urban density, is largely settled. What comes next is the vertical differentiation era: fashion, beauty, medicine, electronics, and pet care, each offering the same speed promise with category-specific experience design.

ZILO’s funding positions it as the first institutional-scale bet on fashion as a standalone vertical. If the model works, it becomes the template for every other vertical: a team with deep category expertise, a supply-side network built for the category’s specific needs, and delivery infrastructure borrowed from the horizontal platforms that already paid to build it.

For Indian founders, the medium-term implication is significant. The infrastructure Peak XV waited to see built is now available to anyone. The consumer habit that Blinkit spent five years forming is now a starting condition, not a prerequisite to build. The window for vertical quick-commerce bets is open. Peak XV’s move signals that the best investors believe it is open right now.

The bottom line

Peak XV did not bet on quick commerce when everyone else did. It waited for the category to prove itself, then bet on what comes next. That is not caution. That is precision.

Key takeaways

- Peak XV Partners made its first quick-commerce investment in February 2026 by leading a $15.3 million Series A in ZILO, a Mumbai-based fashion startup delivering branded apparel in under 60 minutes with home trials and instant returns (YourStory, February 2026).

- ZILO is founded by ex-Flipkart and Myntra executives Padmakumar Pal and Bhavik Jhaveri, whose institutional knowledge of Indian fashion retail is the core competitive moat.

- Peak XV’s deliberate absence from quick-commerce round one signals a thesis: the infrastructure era is over, and the vertical category era has begun.

- India’s quick-commerce market grew from $0.5 billion in FY22 to $3.3 billion in FY24, creating the consumer habit and infrastructure that vertical players like ZILO now build on (Outlook Business, 2025).

- The second wave of Indian quick commerce will be won by whoever builds the best vertical experience on top of delivery infrastructure that Blinkit and Zepto already paid to create.

Conclusion

The Peak XV-ZILO round is not primarily a story about a $15.3 million investment. It is a thesis statement from India’s most active venture firm about where value creation in quick commerce will come from next.

Quick commerce round one produced the infrastructure and the consumer behaviour. Quick commerce round two is about vertical experience design: categories where speed delivery creates a qualitatively different product, not just a faster version of the same one. Fashion, with its inherent try-before-you-buy problem and emotional purchase dynamics, is a structurally strong candidate for the first major vertical winner.

For Indian founders building in adjacent spaces, the timing matters. The dark store infrastructure exists. The consumer habit is formed. The institutional capital is beginning to identify vertical quick-commerce as a real category. The window for building vertical quick-commerce businesses with strong founder-market fit is open in 2026 in a way that it was not in 2022.

Peak XV waited precisely for this moment. The round is worth paying attention to not just for what it funds, but for what it signals about what comes next.

TFN LENS

Peak XV’s ZILO bet is directly instructive for Indian founders in a way that most global VC signals are not, because the infrastructure it is building on is Indian infrastructure, built for Indian consumers, by Indian companies.

The lesson is not to build a fashion quick-commerce startup. The lesson is to find the vertical where Indian consumer behaviour has already been formed by someone else’s capital investment, and where deep category expertise creates a moat that capital alone cannot replicate. That combination, formed behaviour plus domain expertise plus a supply-side network the horizontal players cannot quickly match, is what Peak XV is paying $8 million to back.

The same pattern is available in beauty, medicine, pet care, and electronics. The infrastructure exists. The behaviour exists. The question is which founding team has the category knowledge to build the right product on top of it.

Building something of your own? Follow The Founder Nation and NamasteVC for curated startup funding news, grant alerts, and founder stories from India’s startup ecosystem, delivered straight to your feed, every week.

Frequently asked questions

What is Peak XV Partners?

Peak XV Partners is the India and Southeast Asia arm of the Sequoia network, rebranded from Sequoia Capital India in 2023. The firm manages over $10 billion in AUM and has investments in approximately 70% of India’s unicorns (Business Standard, December 2025). It made 81 investments in 2025 alone (Tracxn, 2026), making it India’s most active venture firm by deal count.

What is ZILO?

ZILO is a Mumbai-based fashion quick-commerce startup founded in 2025 by Padmakumar Pal and Bhavik Jhaveri, both former executives at Flipkart and Myntra. The company delivers on-trend clothing from 200-plus brands in under 60 minutes with home trial included and instant returns available. Celebrity stylist Anaita Shroff Adajania serves as Style Director and equity partner.

Why did Peak XV not invest in Blinkit or Zepto?

Peak XV has not publicly stated a specific reason for staying out of the first quick-commerce wave. The firm’s investment pattern suggests it preferred to wait until the infrastructure investment had proven consumer demand and the next layer of value creation, vertical category businesses, became visible.

How big is India’s quick-commerce market?

India’s quick-commerce market reached $3.3 billion in FY24, up from $0.5 billion in FY22 (Outlook Business, 2025). The market is concentrated in major metros, with Blinkit holding approximately 46% share across its 2,243 dark stores.

Who are ZILO’s competitors in fashion quick commerce?

ZILO competes with other fashion quick-commerce startups including Slikk, KNOT, and Klydo. It also faces potential competition from horizontal quick-commerce platforms like Blinkit and Zepto if they choose to add fashion SKUs at scale. ZILO’s differentiation lies in curated brand selection, home trial capability, and the founder team’s deep Indian fashion commerce expertise.

What does Peak XV’s quick-commerce bet mean for other Indian startups?

It signals institutional appetite for vertical quick-commerce businesses built on proven delivery infrastructure. Founders with deep category expertise in fashion, beauty, medicine, or electronics who can design a category-specific experience on top of existing last-mile infrastructure have a real funding window in 2026.

©️ The Founder Nation | All rights reserved | Written by TFN Research Desk | Word count: ~3,357| Read time: ~18 minutes |

{kind=link}