Every funding round ends with a celebration. Then the lawyers show up.

The Shareholders’ Agreement, or SHA, is the document that most founders sign without fully reading and most investors quietly rely on to protect everything. It is not the most glamorous part of building a startup. It is, however, the most consequential.

Disputes between co-founders are one of the top reasons early-stage startups fail in India. Disagreements between founders and investors have killed companies that were otherwise on trajectory. In almost every case, the problem was not that relationships broke down. The problem was that nobody had written down what would happen when they did.

The SHA is that document. Here is what it actually says, who it protects, and what you need to fight for before you sign it.

What an SHA Is and What It Is Not

A Shareholders’ Agreement is a private, legally binding contract between the shareholders of a company. It is not filed with the Registrar of Companies. It does not become a public record. That privacy is the point.

The Articles of Association, the AoA, is the statutory document that governs the company. It is public and filed with the RoC. But the AoA is a blunt instrument. It cannot handle the nuance of a three-way co-founder equity split, the mechanics of a liquidation waterfall, or what happens when a founder walks out eighteen months after Series A.

The SHA fills that gap. It governs how shareholders interact with each other and with the company across three categories of situation: ordinary governance, transfers of shares, and exit events.

One critical point that founders routinely miss: the SHA must be mirrored in the AoA to be fully enforceable against the company. Signing the SHA and leaving the AoA unchanged creates a conflict that courts will resolve against whichever party is trying to enforce the SHA provision. Your lawyers should amend the AoA at closing.

The Clauses That Actually Decide the Outcome

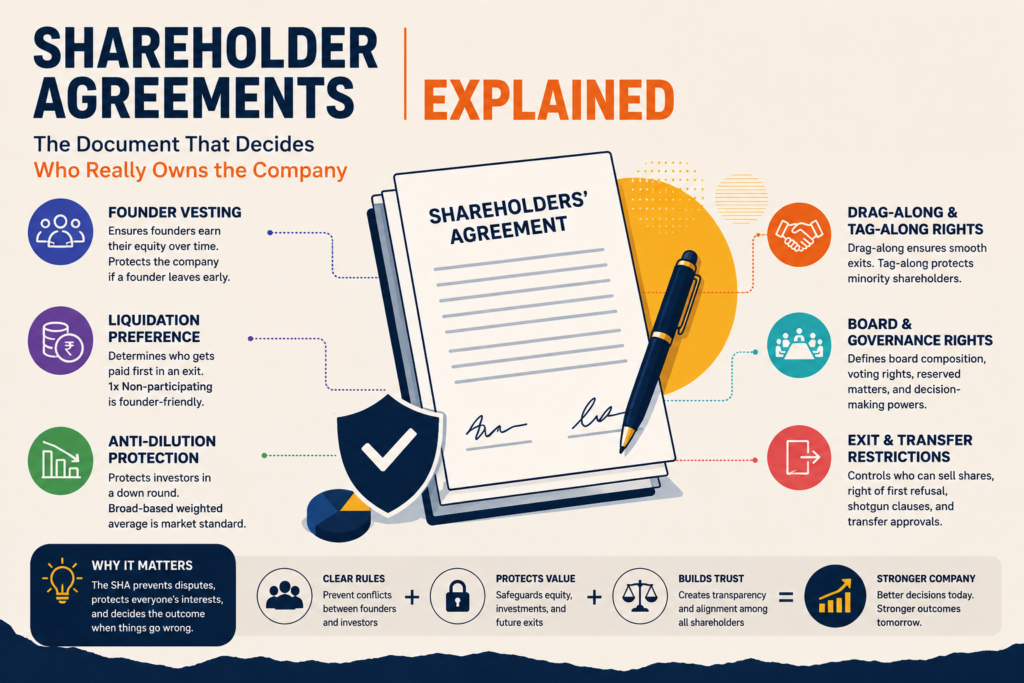

Founder Vesting

Vesting is the mechanism by which founders earn their shares over time rather than owning them outright from day one. The standard structure in India is a four-year vesting schedule with a one-year cliff. No shares vest in the first twelve months. After the cliff, twenty-five percent vests at once. The remaining seventy-five percent vests monthly or quarterly over the following three years.

This protects all shareholders. If a co-founder leaves after eight months, a company that has given away thirty percent of its equity on the cap table but got four months of work cannot raise a credible Series A. Vesting solves that.

What founders need to watch are the leaver provisions. Good leaver treatment, typically defined as resignation with notice or departure due to death or disability, allows a departing founder to keep their vested shares. Bad leaver treatment, which covers termination for cause or resignation without notice, can allow the company to buy back vested shares at face value or a heavy discount.

The problem is that bad leaver definitions are often written broadly enough that a legitimate disagreement between founders can be characterised as cause. Review these definitions line by line.

Liquidation Preference

Liquidation preference determines who gets paid first and how much when the company is sold, merged, or wound down. It is an investor protection. It is also the clause most likely to surprise founders at the exit table.

A 1x non-participating liquidation preference means investors get back their invested capital before founders receive anything. After that, the remaining proceeds are distributed to all shareholders based on their shareholding. This is market standard in India at seed and Series A, and it is fair.

A participating liquidation preference means investors get their capital back first and then continue to participate in the remaining distribution alongside everyone else. This is a double-dip. On a modest exit, it can leave founders with almost nothing.

To illustrate: a Series A investor puts in ₹10 crore at a 2x participating preference. The company is acquired for ₹50 crore. The investor takes ₹20 crore first, then continues to participate on their pro-rata basis in the remaining ₹30 crore. Founders absorb that math.

Push for 1x non-participating as a firm position. It is the most founder-friendly structure an institutional investor in India will typically accept.

Anti-Dilution Protection

When a startup raises a subsequent round at a lower valuation than the previous one, a down round, existing investors lose value relative to their original entry. Anti-dilution provisions protect investors from this by adjusting their conversion price.

Two flavours exist. Broad-based weighted average calculates a new conversion price that takes into account all outstanding shares, including options and warrants. The adjustment is proportional and reflects the actual economic damage of the down round. This is the market standard in India and the version founders should accept.

Full ratchet reprices the investor’s entire holding to the new, lower price. It is punitive. A full ratchet in a significant down round can hand investors a massively increased equity stake at the founder’s expense. If an investor insists on full ratchet, negotiate a sunset clause and a pay-to-play provision as minimum safeguards.

Drag-Along and Tag-Along Rights

Drag-along allows a majority of shareholders, typically the investors alone or investors and founders together, to compel minority shareholders to join a sale of the company on the same terms. This ensures that a buyer can acquire 100% of the equity without a minority holdout blocking the deal.

Tag-along protects minority shareholders. If a majority shareholder is selling, minority shareholders have the right to sell alongside them on the same terms and at the same price, rather than being left behind in a company with a new controlling shareholder they did not choose.

Both are necessary. The negotiation is in the trigger. Founders should insist that drag-along requires consent from both investor majority and founder majority. An SHA that allows investors alone to drag founders into a sale they oppose is a problem.

Reserved Matters

Reserved matters are the list of corporate decisions that require investor consent before the company can act. Common items include raising new capital, changing the business model, making acquisitions above a threshold, hiring or firing C-suite executives, and related party transactions.

The risk is scope creep. Institutional investors, particularly growth-stage funds and foreign PE players, sometimes push for reserved matters lists that run to forty items and effectively give them a veto over operating decisions. Founders should resist this. The list should be limited to genuinely material, infrequent decisions. Anything that makes it impossible to run the company without calling an investor vote is a governance problem waiting to happen.

SHA vs. Founders’ Agreement: What Changes After Investment

| Provision | Founders’ Agreement | SHA Post-Investment |

| Equity splits | Core focus | Incorporated and updated |

| Founder vesting | Often included | Formalised with leaver terms |

| Board composition | Informal | Investor director rights specified |

| Anti-dilution | Not applicable | Added for investor protection |

| Liquidation preference | Not applicable | Negotiated per round |

| Dispute resolution | Often vague | Arbitration with Indian seat |

A Founders’ Agreement is typically superseded by the SHA once institutional capital enters. If you have a Founders’ Agreement, do not assume its terms carry forward automatically. They need to be reviewed and incorporated explicitly.

The Mistakes That Cost Founders the Most

Using an unaltered template is the most common. Every SHA is a negotiation that reflects the specific cap table, the specific investors, and the specific deal terms. A template from the internet does not know any of that.

Signing without amending the AoA is the second. Key SHA protections, including transfer restrictions and board rights, need statutory backing. Without AoA alignment, a counterparty can challenge enforceability.

Ignoring the reserved matters list at seed stage is the third. Founders who are grateful to close their first round often sign reserved matters provisions they would never accept at Series A. Those provisions persist into subsequent rounds unless renegotiated.

Failing to update the SHA when new investors join is the fourth. Each round typically brings new rights and preferences. An outdated SHA that does not reflect the current cap table creates conflicts at the worst possible time.

The Take Nobody Will Say Out Loud

The SHA is framed as a governance document. It is actually a power map.

Every clause in an SHA answers one question: when things go sideways, who wins? The reserved matters list decides who controls the company day to day. The liquidation waterfall decides who makes money at exit. The drag-along trigger decides whether founders have a say in the sale of what they built.

Most founders negotiate the valuation hard and accept the SHA as presented. That is the wrong priority order. A high valuation with a participating preference and full ratchet anti-dilution can deliver less money to the founders than a lower valuation with clean terms.

Read the SHA before you sign it. Then read it again with a lawyer who has no incentive to close the deal quickly. The celebration can wait forty-eight hours.

Frequently Asked Questions

What is the difference between an SHA and an AoA? The Articles of Association is a statutory document filed with the Registrar of Companies that governs the internal management of the company. It is public. The SHA is a private contract between shareholders that adds detail the Companies Act does not prescribe, including vesting schedules, anti-dilution rights, and exit mechanics. For SHA provisions to be fully enforceable against the company, the AoA must be amended to reflect them.

Do co-founders need an SHA before raising money? Strictly speaking, a Founders’ Agreement covering equity splits, vesting, roles, and departure terms is sufficient before the first external investor comes in. But converting that into a proper SHA early, even at the friends-and-family stage, avoids the situation where ambiguous verbal understandings have to be untangled under pressure at due diligence.

What does 1x non-participating liquidation preference mean in plain terms? It means that in a sale or wind-down, the investor gets back the amount they invested before founders and other ordinary shareholders receive anything. After the investor’s capital is returned, the remaining proceeds are split based on shareholding. Non-participating means the investor does not also participate in the residual distribution. This is the most founder-friendly version of liquidation preference that institutional investors in India typically accept.

Can a founder be forced to sell their shares under a drag-along clause? Yes, if the drag-along threshold is met. The threshold is negotiable. A well-drafted SHA for founders should require that drag-along can only be triggered with both investor majority and founder majority consent, so that investors cannot force a sale that founders collectively oppose. Review who controls the drag-along trigger before signing.

What happens to my unvested shares if I leave the company? This depends on whether you are classified as a good leaver or a bad leaver under the SHA. Good leavers typically keep their vested shares. Bad leavers may be required to sell vested shares back to the company at face value or a discount. The definitions of good leaver and bad leaver are negotiable and vary significantly between agreements. Review these definitions carefully, as they determine your financial outcome in a forced departure scenario.

Is an SHA enforceable in India? Yes. Indian courts have consistently held SHAs to be binding contracts under the Indian Contract Act, 1872. Provisions including drag-along, tag-along, and right of first refusal have been enforced in civil and arbitration proceedings. The Amazon vs. Future Group dispute is the most high-profile example of SHA rights being litigated and enforced in India, including enforcement of contractual rights of first refusal that blocked a major acquisition. Arbitration with an Indian seat is the recommended dispute resolution mechanism for SHA disputes between Indian residents.

When should the SHA be updated? At every priced funding round, without exception. New investors bring new rights and preferences that must be incorporated. An SHA that reflects the seed round cap table but not the Series A terms creates conflicts that are expensive to resolve later.

Stay in the Loop

For more stories, breakdowns, and unfiltered takes on what is really happening in Indian and global business and tech, follow TheFounder Nation.

Instagram Handle : https://www.instagram.com/thefoundernation?igsh=MTZobDUwc2xqZWdhOA==

We cover what the mainstream business press won’t.

© TheFounder Nation | All rights reserved Word count: ~1,500 | Read time: ~6 minutes Primary keyword: shareholder agreements explained | Secondary: SHA India startup, SHA clauses founders, liquidation preference India, drag-along tag-along rights India, founder vesting SHA, anti-dilution clause startup India, reserved matters SHA, SHA vs AoA India

{kind=link}