Written by TFN Research Desk | covering startups, technology, venture capital, and business strategy.

While Indian startup funding fell 17% in 2025, the country climbed to the world’s third-largest funded tech ecosystem, and the founders driving that paradox did it by raising less, not more.

The founders who raised the most in 2021 are the ones who suffered the most in 2024. The smart money learned that lesson the hard way. What replaced the raise-at-any-cost era is more interesting and more durable than anything the boom years produced.

Topic tags: Startup Strategy • Sector Analysis • Venture Capital • Indian Startups • Fundraising

The era of raise at any cost is over

In 2021, an Indian startup raising $50 million at a $500 million valuation was considered a success story.

By 2024, many of those same startups were doing down rounds, mass layoffs, and quiet pivots, trying to make businesses that had been valued on growth projections actually work on unit economics.

The hangover was brutal. And the founders who watched it happen from the sidelines took notes.

Entering 2026, a new posture has emerged across India’s startup ecosystem. Not pessimism. Not fear. Deliberate caution: a strategic recalibration that is producing stronger companies than the boom years ever did.

Why this story matters

India’s startup ecosystem is entering its most consequential phase since the smartphone unlocked consumer internet. The companies that navigate this period well will define the country’s next generation of durable technology businesses.

The shift toward fundraising caution is not a local anomaly. It mirrors the recalibration that happened in the US market after the dot-com correction, when the companies that survived by being capital-efficient went on to outlast and outperform their better-funded peers.

For founders building today, understanding why the best operators are raising less and more deliberately is not optional context. It is the strategic playbook for the next five years. [INTERNAL LINK: “India unicorn sector analysis 2025-2026”] covered how these same dynamics are reshaping which sectors attract institutional capital. And [INTERNAL LINK: “venture debt vs equity dilution: what Indian founders should know”] goes deeper on the financing instruments now replacing traditional equity rounds at the growth stage.

Quick facts

| Metric | Value | Source |

|---|---|---|

| Indian startup funding (2025) | $10.5 billion | Tracxn India Tech Annual Funding Report 2025 |

| Year-on-year change | Down 17% from $12.7 billion in 2024 | Tracxn |

| Seed funding drop | Down 30% to $1.1 billion | Tracxn via TechCrunch |

| Investor participation | Down 53% (3,170 vs approximately 6,800 a year earlier) | Tracxn via TechCrunch |

| New unicorns in 2025 | 5 confirmed; up to 11 by some counts | Tracxn and Hurun |

| Combined unicorn valuation | Over $365 billion | Hurun India Unicorn Index 2025 |

| India’s global ranking | 3rd largest funded tech ecosystem, behind US and UK | Tracxn |

| H1 2025 funding | $4.8 billion, down 25% year-on-year | Tracxn H1 2025 Report |

Background

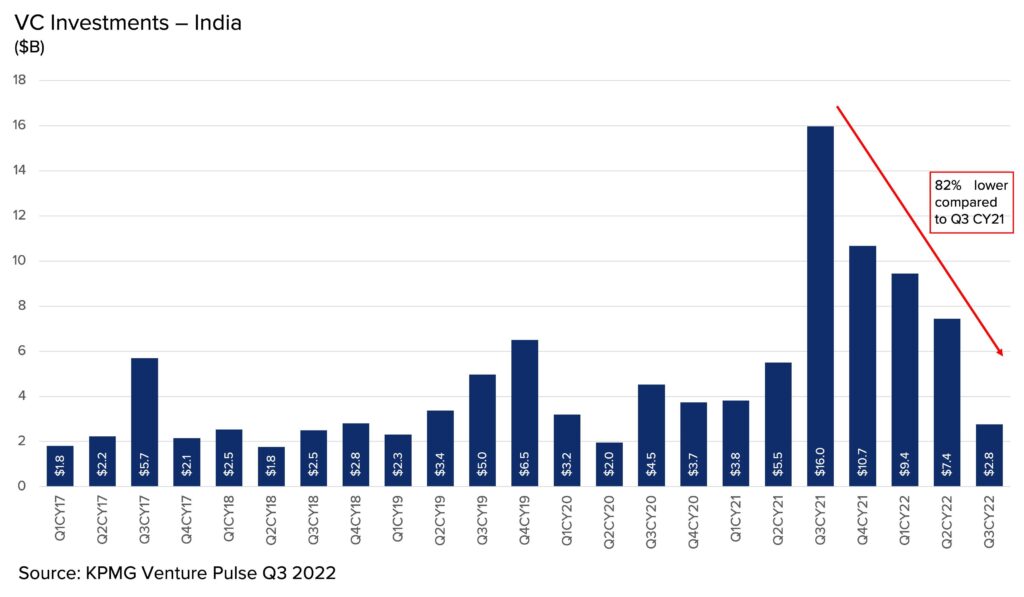

The funding winter of 2022-2023 was not the beginning of this story. It was the consequence of the story that came before it.

Between 2020 and 2022, global capital flooded into emerging market tech at a scale the ecosystem had never seen. Zero interest rates pushed institutional investors toward higher-yield alternatives. The result was a compression of diligence timelines, inflated entry valuations, and a generation of startups that raised more capital than their unit economics could justify.

When interest rates rose globally, the correction was swift and indiscriminate. Companies that had raised at 100x revenue found themselves unable to justify the next round. Investor portfolios that had marked up aggressively were forced to mark down. The secondary effects spread through the entire ecosystem, affecting even capital-efficient companies whose investors had become risk-averse.

India’s startup ecosystem bore a disproportionate portion of this correction because it had participated disproportionately in the boom. Unicorns created on paper valuations in 2021 found themselves in 2023 renegotiating burn rates, cutting headcount, and explaining to boards why the growth curves of two years ago were no longer achievable.

What emerged on the other side was not a weakened ecosystem. It was a restructured one, where the founders who survived had been stress-tested in ways no due diligence process can replicate.

Timeline: how Indian startup caution developed

| Year | Milestone |

|---|---|

| 2020 | Global zero interest rate environment accelerates VC deployment into emerging markets, including India |

| 2021 | Indian startup funding peaks. Multiple $100M-plus rounds closed in weeks. Unicorn creation accelerates. |

| 2022 | Global interest rate hikes begin. Foreign mega-fund appetite for India cools sharply. Down rounds start appearing. |

| 2023 | The funding winter. Indian startup layoffs reported across edtech, fintech, and consumer internet. Founders begin prioritising runway over growth. |

| 2024 | Funding stabilises at $12.7 billion. Domestic investors and family offices fill the gap left by global funds. Unit economics become the primary investor conversation. |

| 2025 | Funding reaches $10.5 billion (down 17%). Investor count falls 53%. Seed funding drops 30%. India climbs to third-largest funded tech ecosystem globally. IPO pipeline grows to approximately 20 startups. |

| 2026 | Capital discipline is now the default founder posture. Venture debt adoption rises. Runway targets of 18 to 24 months before approaching investors become standard. |

How it happened

Shift 1: The 2021 cohort became a cautionary tale

The founders who watched the 2021 boom turn into the 2023 correction did not need a framework for understanding what went wrong. They watched it happen to people they knew.

The pattern was consistent. A startup raises at an aggressive valuation tied to a forward revenue multiple. It deploys capital on growth, hiring, and customer acquisition subsidies. When the next round arrives, the growth projections have not materialised and the multiple has compressed. The options at that point are brutal: a down round that signals distress publicly, a bridge that extends the pain, or a shutdown.

The founders who watched this cycle from the sidelines made a different calculation. They decided the valuation at which you raise is not a badge of progress. It is a ceiling you must grow above or a trap you grow into.

Shift 2: Investor participation narrowed, and quality improved

As global mega-funds pulled back, the composition of Indian startup investors shifted. Approximately 3,170 investors participated in Indian startup rounds in 2025, compared to roughly 6,800 the year before, a 53% reduction (Tracxn, 2025).

That contraction might read as bad news. In practice, it filtered out the tourists. The investors who stayed through the correction were the ones with real conviction in Indian consumer and B2B markets, deeper operational relationships with founders, and longer time horizons than the global growth funds that had rushed in during 2021.

The result: founders raising in 2025 and 2026 are dealing with investors who know the ecosystem well, expect real unit economics, and are less likely to push for unsustainable growth targets that set up the next correction.

Shift 3: The IPO pipeline replaced offshore exit narratives

One of the most significant structural shifts in Indian startup thinking since 2023 is the emergence of public markets as a realistic exit path. Approximately 20 startups were preparing for Indian public listings as of 2025 (TICE News, 2025).

This changes how founders think about capital from the beginning. A company building toward an Indian IPO operates differently than one building toward a Series D or a strategic acquisition. It needs clean governance from the start. It needs auditable financial reporting. It needs the kind of operational discipline that does not develop overnight.

Founders who know they are building toward public markets have less incentive to accept capital from investors pushing for growth at any cost. The governance requirements of a public listing are incompatible with the slash-and-burn growth models that characterised the 2021 boom.

The strategy behind the success

The insight at the centre of Indian founders’ cautious approach is simple: valuation is a vanity metric until it becomes a trap.

The founders driving this recalibration understood that the higher your valuation at entry, the harder it becomes to justify at the next round. A startup that raises at reasonable multiples with strong unit economics has room to grow at its own pace, respond to market shifts, and maintain negotiating leverage with investors. A startup that raises at 100x revenue needs everything to go exactly right, forever.

Caution is not timidity here. It is optionality. Founders who build to 18 to 24 months of runway before approaching investors enter conversations from a position of strength, not desperation. That shifts every dynamic in the room.

By the numbers

| Metric | Value | Source | Why it matters |

|---|---|---|---|

| Total startup funding (2025) | $10.5 billion | Tracxn | Down 17%, but quality of fundable companies is higher |

| Seed funding decline | 30% to $1.1 billion | Tracxn via TechCrunch | Early-stage scrutiny is significantly sharper than 2021 |

| Investor participation drop | 53% fewer investors | Tracxn via TechCrunch | Capital is concentrating in fewer, higher-conviction hands |

| IPO pipelines | Approximately 20 startups preparing for listings | TICE News, 2025 | Founders are building for public markets, not VC exit narratives |

| New unicorn count (2025) | 5 confirmed; up to 11 by some counts | Tracxn, Hurun | Unicorns still being created, just on more defensible foundations |

Comparison table: 2021 boom-era founders vs 2026 discipline-first founders

| Dimension | 2021 cohort | 2026 cohort |

|---|---|---|

| Primary fundraising goal | Raise as much as possible at peak valuation | Raise the minimum needed for the next defined milestone |

| Typical runway before raise | 6 to 9 months (raising from near-empty) | 18 to 24 months (raising from a position of strength) |

| Valuation anchor | Forward revenue multiples (100x and above common) | Current revenue multiples with a defensible growth curve |

| Growth model | Subsidised customer acquisition; unit economics secondary | Unit economics positive at product level before scaling |

| Exit orientation | US or international VC-led exit via strategic acquisition | Indian public markets via NSE/BSE listing |

| Investor relationship | Take any term sheet from a recognised name | Selective; prefer domain-specialist investors with operator networks |

| Financing instruments used | Primarily equity (Seed, Series A through D) | Mix of equity plus venture debt at growth stage to limit dilution |

| Governance and reporting | Built reactively as investor requirements demand | Built proactively from early stage as IPO preparation |

What competitors missed

The global venture ecosystem misread India’s 2025 funding decline as evidence that the ecosystem was contracting. When headline numbers fell, the assumption was that India’s startup moment was stalling.

What was actually happening: the ecosystem was maturing. The companies getting funded in 2025 were fundamentally more viable than the ones that raised in 2021. Investors who stayed in India through the correction are now holding positions in businesses with real revenue, real margins, and real paths to public markets.

The misread was partly structural. Global funds that had deployed into India during the boom were themselves under pressure from LPs reassessing emerging market allocations. Their reduced activity in India was not a judgment on India’s fundamentals. It was a consequence of their own portfolio stress. covers this mechanic in more detail.

The founders and domestic investors who understood this distinction did not panic. They bought time when others were selling it.

Risks and challenges

- The contraction in seed funding is not only a quality filter. It is also making it harder for first-time founders from non-metro cities and non-IIT backgrounds to access early capital, since the investors who remain are concentrated around established networks.

- Venture debt, while useful for limiting dilution, carries real repayment obligations. Founders adopting it need to model their cash flow with more precision than equity financing requires, and a revenue shortfall has immediate consequences.

- The IPO pipeline of 20 startups in 2025 assumes a public market appetite for tech listings that has not always been consistent. A poor performance by early movers could freeze the pipeline for those behind them.

- Global macro conditions remain a risk. A stronger dollar or a global risk-off period could further reduce foreign institutional participation in Indian startup rounds, independent of how strong individual companies are.

- Capital discipline taken too far can also limit growth. Companies that are so conservative about raising that they underinvest in product or distribution can be outpaced by well-funded competitors when market windows are time-sensitive.

What founders can learn

- Build for 18 to 24 months of runway before approaching investors. Desperation is the most expensive negotiating position there is.

- Treat unit economics as a document you could present publicly at any time. If you cannot explain your contribution margin clearly to yourself, you cannot defend your valuation to an investor.

- Explore venture debt before equity dilution at the growth stage. Debt costs money in interest. Dilution costs control permanently.

- Do not raise at inflated valuations to signal progress. The valuation you raise at today is the floor you must defend at the next round. If you miss it, the down round costs more than the premium you captured.

- Start building IPO-ready governance habits from day one, even if a listing is five years away. The discipline required for public markets cannot be installed quickly.

Expert analysis

Bull case: India’s startup ecosystem in 2026 and beyond will produce a cohort of companies that are fundamentally more investable than those of the 2021 boom. Better unit economics, real revenue, a growing domestic IPO pipeline, and a surviving founder base that has been stress-tested by an actual correction. The pain was productive, and the companies that emerged from it are structurally more durable.

Bear case: Global macro uncertainty, a stronger dollar, and continued caution from foreign institutional investors could extend the funding compression into 2027. Startups that are capital-efficient may still find their growth limited if the exit environment for investors does not improve. The domestic IPO market has not yet absorbed enough tech listings to prove it can handle the pipeline that is forming behind it.

Contrarian view: The real story of Indian startup caution is not about founders at all. It is about the LPs (limited partners) behind Indian venture funds. When global LPs reduce commitments to emerging market funds, the entire food chain tightens. Founder discipline is partly a response to a structural reduction in available capital, not purely a strategic choice. The founders who look most disciplined may simply be the ones who have adapted most efficiently to an environment where capital is genuinely scarcer.

Future outlook

India’s startup ecosystem is at an inflection point that closely resembles the US market in 2002 to 2004, in the years after the dot-com correction compressed valuations and forced genuine business model discipline on surviving companies.

What followed that US correction was the most durable cohort of technology companies in modern business history. The companies built in the scarcity years outperformed those built in the boom years, because they never developed the muscle memory of depending on capital to simulate traction.

The Indian market is now producing the same stress-tested cohort. The 20-company IPO pipeline forming in 2025 will begin resolving in 2026 and 2027. How those listings perform will determine whether domestic public markets can replace the offshore exit narratives that dominated Indian startup strategy for the previous decade.

If they perform well, the feedback loop will be transformative. Founders will have a domestic path to liquidity. Investors will have exits that do not depend on US-market appetite for Indian tech acquisitions. And the ecosystem will have a valuation anchor rooted in real earnings rather than forward projections from capital markets that are 10,000 kilometres away.

The bottom line

The best Indian founders in 2026 are not raising less because they have smaller ambitions. They are raising less because they understand that the capital structure of your company is a competitive variable, not just a financial necessity. The ones who get this right will not just build better businesses. They will build businesses that do not need the next boom to survive the next correction.

Key takeaways

- Indian startup funding fell 17% to $10.5 billion in 2025, but the ecosystem climbed to the third-largest funded tech ecosystem in the world, overtaking Germany and China.

- Investor participation dropped 53%, signalling consolidation around fundamentals rather than a collapse of confidence.

- The best founders are treating capital discipline as a competitive advantage, not a constraint imposed by a difficult market.

- A comparison of the 2021 and 2026 founder cohorts shows structural differences in runway strategy, valuation approach, growth models, and exit orientation, not just a change in sentiment.

- India’s funding timeline from 2020 to 2026 is a complete arc from boom to correction to maturation, and the companies building through the maturation phase are structurally more defensible than those born in the boom.

- IPO pipelines are growing as founders build for public markets rather than VC-driven exit narratives.

- The funding winter of 2022-2023 produced a generation of Indian startups with stronger unit economics, longer runways, and more defensible growth models than anything the 2021 boom created.

Conclusion

The era of raise at any cost is not coming back. That is not a loss for the Indian startup ecosystem. It is the correction that the ecosystem needed.

The founders building today are operating in a market where capital is a tool rather than a signal. Where a large round earns scrutiny, not applause. Where the question investors are asking is not “how fast can you grow?” but “what does this look like when it doesn’t need us anymore?”

That is a harder environment to raise in. It is a far better environment to build in.

The companies that emerge from this phase will not have been sheltered from the discipline of real markets. They will have been built inside it. That is the competitive advantage the 2021 cohort never had, and the one the 2026 cohort will carry for the life of their companies.

TFN LENS

The real lesson from India’s fundraising recalibration is not that the funding market is harder.

The real lesson is that the best founders have stopped treating fundraising as a milestone. They are treating it as a tool, one they reach for carefully and use precisely.

The 2021 cohort raised money because they could. The 2026 cohort is raising money because they need to, on terms they control, with businesses that do not need the round to survive.

That is not caution. That is power.

Building something of your own? Follow The Founder Nation and NamasteVC for curated startup funding news, grant alerts, and founder stories from India’s startup ecosystem, delivered straight to your feed, every week.

Frequently asked questions

Why are Indian founders raising less money in 2025 and 2026?

The primary reason is the hangover from the 2021-2022 boom, when many startups raised at valuations that their unit economics could not support. When those companies faced down rounds and layoffs in 2023 and 2024, the founders watching drew a direct lesson: the valuation you raise at is a floor you must defend, not a ceiling you grow into. Caution is now the rational response to having watched the consequences of the alternative.

Did Indian startup funding collapse in 2025?

Not by any structural measure. Funding fell 17% to $10.5 billion, and investor participation dropped 53%. But India still ranked as the third-largest funded tech ecosystem in the world, and the country added between 5 and 11 new unicorns depending on the counting methodology. The headline decline reflects a quality filter more than an ecosystem contraction.

What is the difference between the 2021 and 2026 Indian founder fundraising approach?

The key differences are in runway strategy (6 to 9 months before raising in 2021 vs 18 to 24 months in 2026), valuation anchor (forward multiples vs current revenue multiples), and exit orientation (US-driven acquisition vs Indian public markets). The 2026 approach treats capital as a tool rather than a milestone.

Why did seed funding fall 30% in India in 2025?

Seed funding declined as early-stage investors applied significantly more scrutiny than in previous years. The investors who stayed in India after the correction are deploying more slowly and more selectively, particularly at the earliest stages where the failure rate is highest. The reduction in global LP commitments to emerging market funds also reduced the total pool of early-stage capital available.

What is the venture debt trend among Indian startups?

An increasing number of Indian startups at the growth stage are exploring venture debt as an alternative to equity dilution. Venture debt allows a company to extend its runway or fund a specific initiative without giving up equity or accepting a valuation mark at an inopportune time. The trade-off is that debt has real repayment obligations, so it requires more precise cash flow management than equity financing.

How many Indian startups are preparing for IPOs?

As of 2025, approximately 20 Indian startups were reported to be preparing for public listings on Indian exchanges (TICE News, 2025). This pipeline represents a structural shift in how Indian founders think about exits, moving away from dependence on offshore acquisition markets or US-listed vehicles toward domestic capital markets.

Official & Primary Sources

- Tracxn India Tech Annual Funding Report 2025

- Tracxn India Tech Annual Funding Report 2025 (Press Release)

- Tracxn India Tech Semi-Annual Funding Report H1 2025 (PDF)

- Hurun India Startup Reports (includes Unicorn reports)

©️ The Founder Nation | All rights reserved | Written by TFN Research Desk | Word count: ~3519 | Read time: ~19 minutes |

{kind=link}